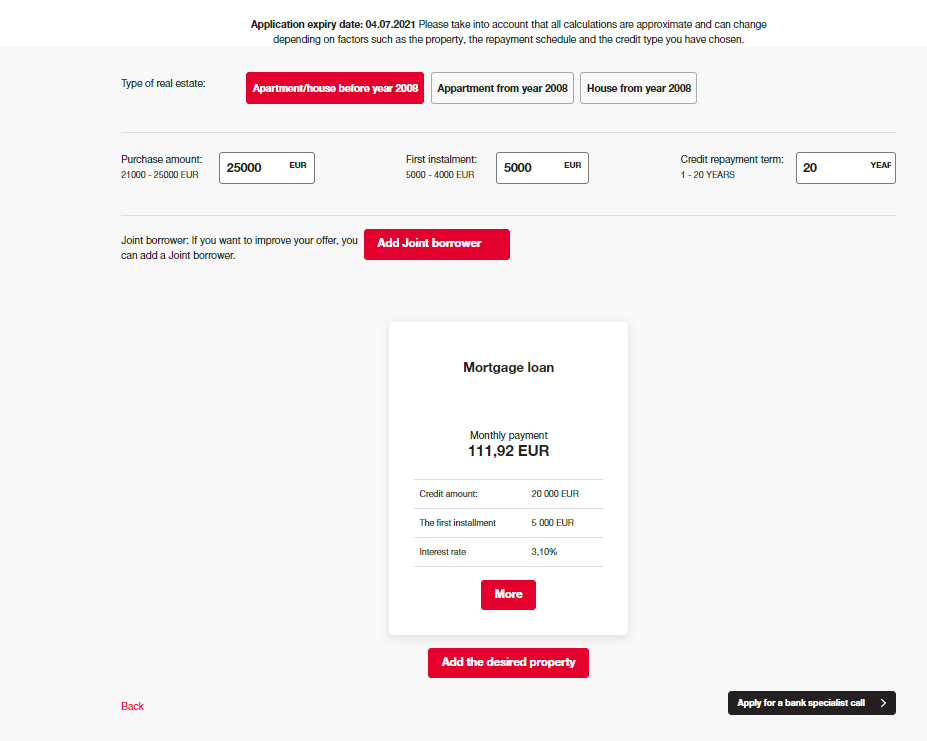

The calculations made using the calculator are of an informative nature and each client's situation is assessed individually.

On our website, we use our own and third-party cookies to provide a better website and online service user experience and offer content and services which interest you, based on your habits. See more in our Cookie Terms and Conditions. You can agree to our use of cookies by selecting Confirm, or reject them by selecting Reject. You can also change or cancel your decision at any time by selecting Cookie Settings. If you choose to reject all cookies, our website will only save the functional cookies necessary for the website to function and be secure, and for which we do not require your permission.